Budgeting 101: How To Start Bossing Your Money Around

I haven’t always had a real budget. Early in my young adult life I would have told you I had a budget because I knew that I had not over drawn my bank account. Even in my early married life our “budget” was simply making sure that we didn’t spend more than we could pay for. However, after about 2 years of following financial guru Dave Ramsey, I now get what a “real” budget is. I’d like to show you what I’ve learned in Budgeting 101. I’m not a financial adviser. I’m simply providing tools for you to use to figure out your own financial goals. If you need financial advice, you should seek the help of a trained financial adviser.

What a real budget looks like:

- Budgeting is not “tracking” your money.

- Budgeting is “planning” your money.

- In essence, budgeting is bossing your money around and telling it exactly what to do in the month to come.

- We are talking micro-managing your money.

- When you get on a real budget, your spending doesn’t control you, you control it.

Where do I start?

- Budgeting starts with sitting down and figuring out where your money has to go each month.

- If you are married, get your spouse involved because it’s important. If you have trouble convincing them, make budget night a fun night. Order pizza and rent a movie upon completion. Budget night doesn’t have to be fight night.

- Set up a budget.

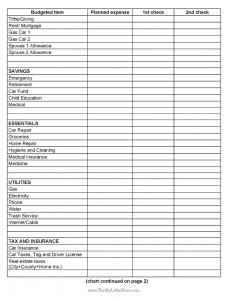

- I have created 2 free printable budget sheets that you can use depending on your situation.

- Budget 2.0= For people who get paid twice a month (click here to print).

- Budget 4.0 = For people who get paid once a week (click here to print).

- My printable budget is the one my family uses to plan and it works great for us (we have a consistent income and pretty basic expenses).

- Print the form and use it as is. You could also use it as guide for making your own electronic spreadsheet. (If you can’t afford Microsoft, go for a free spreadsheet program like LibreOffice. It’s designed by geeks who like software to be free to the world. My husband is one of those kinds of geeks, so we use it for our budgeting!)

- Irregular Income or Big Debts-

- If you have a situation where you have an irregular income, have many debts to pay, or want more advice from a financial mastermind, visit Dave Ramsey’s website, explore and use his free printable budget tools. Look for the “tools” tab.

- If you also are looking on advice for steam rolling your debt situation, get Dave Ramsey’s The Total Money Makeover: Classic Edition: A Proven Plan for Financial Fitness book online or from your local library.

Completing A Budget:

- Once you have either printed the budget above or set up your own spreadsheet, go ahead and start filling in the numbers.

- Go line by line thinking about your own expenses/debts. Fill in the “Planned Expense” column with these numbers. Add any budgeted items that are missing in the blank “Budgeted Item” spaces or ignore the items that don’t apply to your life.

- Now that you have established all the things you spend money on, go line by line and fill in how much you spend each month on all those items.

- Special Line Items- If you are preparing this budget for March and Aunt Sally has a birthday and your BFF is having a baby shower, add those specific things. Tell some of your money to go to gifts for those people.

- Non-monthly expenses- We like to save each month for things that don’t actually happen each month. For example, we figure out how much our car insurance was for the previous 6 months, add a little cushion and then divide by 6 (our car insurance bill comes up every 6 months and we pay in full). Then each month we are telling a portion of our money to go toward our auto insurance. This also works for home owners insurance, car taxes, real estate taxes, subscriptions and any other expense that it broader than a month.

- Expenses that go up and down- There are expenses like gas, electricity and natural gas bills that fluctuate throughout the year. We basically looked at the previous year’s bills, added them up and divided them by 12. Then we got an average cost of that utility to go on.

- Living Month to Month- For people with little to no extra savings or left over money each month, you may not have the luxury of an “average” amount for your utilities. If that’s you, estimate what your monthly expense based on last month’s numbers. When you get to a season change, adjust your amounts to reflect usage rises (such as a cold month, putting more money on your heating bill line to cover increased usage).

- Add up all the items and fill in the “Total Expenses” line at the bottom.

- Fill in your monthly expected “Household Income” under “Planned Expenses” based on how much your expected pay checks add up to.

- Subtract what your spending from what you’re making and put the number beside “Difference between expenses & income”.

- Divide & Conquer- The columns with 1st check, 2nd check or 1st, 2nd, 3rd, 4th check (depending on which budget form you are using) are set up so that you can plan to pay for different expenses out of each check you receive. If your rent is due the first week of the month, you probably want money from your first pay check to go toward that. If your water bill is due at the end of the month, you use your last check for that. If you are new to budgeting, start with making sure you are bringing in enough money period before you start dividing up your pay checks. Start simple. Divide your paychecks up as the last thing that you do with your budget.

Handling Your Budget’s Results:

- Leftovers- If you have extra left over, you need to boss that money around and tell it where to go.

- A good budget doesn’t leave money floating around. It tells that money to go to work somewhere. In this case you may want to put more in retirement or add it to a line item you already created. On the other hand, you may want to send that extra to your “savings” line, “vacation” line or add it to an emergency fund. It’s totally up to you but make it go somewhere.

- Zero’s are good in budgeting- When you complete your budget correctly the difference between your expenses and your income should be $0 because it will mean that every dollar you have taken in, has gone somewhere. Unless you have a negative…

- Negatives: If your spending more than you are making, you have two options: 1) Spend Less. 2) Earn more.

- For some people the answer is simple: spend less.

- For some people who are barely making ends meet by paying for necessities like food, water, shelter: earn more is the difficult answer.

Need To Spend Less?

- If your plan for the coming month shows that you are planning to spend more than you are planning to make, you need to spend less.

- Start at the top of your budget sheet and go line by line defining items that you have control over.

- Things like: eating out, vacations, allowances or anything non-essential to daily survival.

- Play with all those numbers and see if you can get your budget back to zero by eliminating or cutting back how much money you allow to go to those items.

- Credit cards AREN’T YOUR money. That $5,000 credit limit money belongs to a credit card company and they tell that money what to do; not you. Budgeting doesn’t tell your extra expenses to go to your Credit Card. (Don’t believe me? See who has to fight not to pay when someone fraudulently uses your credit card…) As you plan the upcoming month, pretend your credit card doesn’t exist.

- It comes down to what you are literally bringing into your tangible bank account versus what you need to pay for each month.

- Once you do it, you HAVE to stick to it or else you will be in a big mess.

Need To Make More?

- I realize that every single person’s situation is different. I don’t know you. I don’t know your life. I don’t know your situation. I’ve never walked a day in your shoes.

- You are reading this post because the idea of controlling your money interests you, therefore I’m simply giving advice based on my own experience with jobs, money and finance. Take it, leave it or do what you can with it.

- My situation- When my husband and I moved out-of-state, my husband was a full-time student and I could not find a job. With a four-year degree and going on a month without a job offer or any income I had to make a choice. Set my 4 Year Bachelor of Arts Degree pride aside and apply for jobs so that I could pay my bills or allow us to dwindle our savings down to an uncomfortable level. I chose going out and getting a retail job that paid less than my college internship to ensure that we could eat, sleep and survive in our new stage of life. So I took the best job I was offered, worked hard and fought for as many hours as I could get.

- My outcome- 6 months later, I was offered a job in my career field and never stressed too much over finances because I simply did what had to be done, enjoyed the journey and gleaned all I could from my retail job.

- Perspective and attitude can make a big difference in working environments no matter where you find yourself.

- Thoughts for fighting part-timers- If you find yourself working a million part-time jobs, considering finding 1 steady full-time job/ almost full time and fill in the gaps with a part-time jobs.

- Thoughts for “settlers”- If you feel like you are settling for less than your best, take a step back and try changing your perspective. Does the stability and reliability of a steady pay check now set you up to be able to do what you want to do in the future?

- Work Force Misconceptions- As a young adult I found that many of the conceptions I had of the professional world were wrong. I didn’t walk out of college with my 4 year degree and get handed the job of my dreams. I worked many jobs I hated, just to insure that I could do what I wanted in the future.

- 10 years after high school graduation, I’m doing what I really love.

- Foundations- It took years of foundation laying to get where I can do what I love. It also took years of telling my hard-earned, sometimes hard-fought money exactly where I wanted it to go.

- Emergency Funds- An emergency fund never really hurt anyone. If you can get $1,000 saved for some of the emergencies life throws your way, it might help you sleep a little better at night. If you don’t have an emergency fund, consider taking your next tax return or work bonus and throwing it in a savings account or sock drawer for emergencies and skip the new flat screen or family trip to the beach.

Once you have got this part of the system down, check out the next post in this series: Budgeting 102- 4 Ways to Track Your Spending!

I hope that this post and the free printables will help you and your family understand how to start bossing your money around and telling it what to do each month. Please share any thoughts, questions or budgeting advice you may have in the comments section below!

Kim Anderson is the organized chaos loving author behind the Thrifty Little Mom Blog. She helps other people who thrive in organized chaos to stress less, remember more and feel in control of their time, money, and home. Kim is the author of: Live, Save, Spend, Repeat: The Life You Want with the Money You Have. She’s been featured on Time.com, Money.com, Good Housekeeping, Women’s Day, and more!